Retail sales taxes are one of the more transparent ways to collect tax revenue. While graduated income tax rates and brackets are complex and confusing to many taxpayers, sales taxes are easier to understand; consumers can see their tax burden printed directly on their receipts.

In addition to state-level sales taxes, consumers also face local sales taxes in 38 states. These rates can be substantial, so a state with a moderate statewide sales tax rate could actually have a very high combined state and local rate compared to other states. This report provides a population-weighted average of local sales taxes as of January 1, 2022, to give a sense of the average local rate for each state. Table 1 provides a full state-by-state listing of state and local sales tax rates.

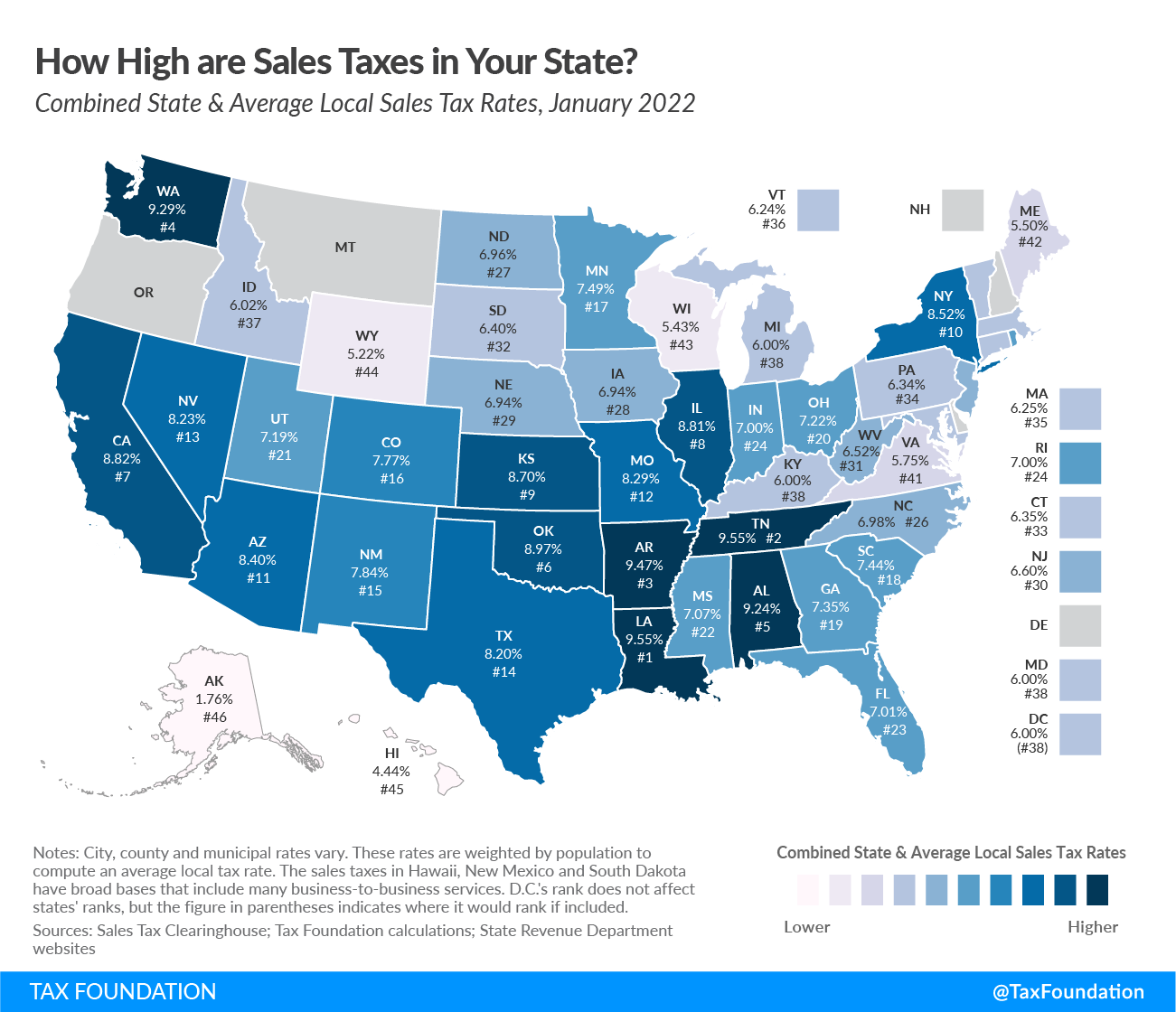

Five states do not have statewide sales taxes: Alaska, Delaware, Montana, New Hampshire, and Oregon. Of these, Alaska allows localities to charge local sales taxes.[1]

The five states with the highest average combined state and local sales tax rates are Louisiana (9.55 percent), Tennessee (9.547 percent), Arkansas (9.48 percent), Washington (9.29 percent), and Alabama (9.22 percent). The five states with the lowest average combined rates are Alaska (1.76 percent), Hawaii (4.44 percent), Wyoming (5.22 percent), Wisconsin (5.43 percent), and Maine (5.50 percent).

California has the highest state-level sales tax rate, at 7.25 percent.[2] Four states tie for the second-highest statewide rate, at 7 percent: Indiana, Mississippi, Rhode Island, and Tennessee. The lowest non-zero state-level sales tax is in Colorado, which has a rate of 2.9 percent. Five states follow with 4 percent rates: Alabama, Georgia, Hawaii, New York, and Wyoming.[3]

No state rates have changed since April 2019, when Utah’s state-collected rate increased from 5.95 percent to 6.1 percent. (The state rate is now officially 4.85 percent, but the state collects an additional 1.25 percent in mandatory taxes that are distributed to local governments, in addition to local option taxes imposed by localities.)[4]

The five states with the highest average local sales tax rates are Alabama (5.24 percent), Louisiana (5.10 percent), Colorado (4.88 percent), New York (4.52 percent), and Oklahoma (4.47 percent).

No states saw ranking changes of more than one place since July.[5] Minnesota moved from 18 th to 17 th highest, largely because of an increase in Washington County’s dedicated Transit Sales and Use Tax from 0.25 to 0.5 percent in October of 2021.[6] Beaufort County, South Carolina, saw the end of its 1 percent transportation tax at the end of 2021, helping improve the state’s rank from 17 th to 18 th .[7]

It must be noted that some cities in New Jersey are in “Urban Enterprise Zones,” where qualifying sellers may collect and remit at half the 6.625 percent statewide sales tax rate (3.3125 percent), a policy designed to help local retailers compete with neighboring Delaware, which forgoes a sales tax. We represent this anomaly as a negative 0.03 percent statewide average local rate (adjusting for population as described in the methodology section below), and the combined rate reflects this subtraction. Despite the slightly favorable impact on the overall rate, this lower rate represents an implicit acknowledgment by New Jersey officials that their 6.625 percent statewide rate is uncompetitive with neighboring Delaware, which has no sales tax.

(a) City, county and municipal rates vary. These rates are weighted by population to compute an average local tax rate.

(b) Three states levy mandatory, statewide, local add-on sales taxes at the state level: California (1%), Utah (1.25%), and Virginia (1%). We include these in their state sales tax.

(c) The sales taxes in Hawaii, New Mexico, and South Dakota have broad bases that include many business-to-business services.

(d) Special taxes in local resort areas are not counted here.

(e) Salem County, N.J., is not subject to the statewide sales tax rate and collects a local rate of 3.3125%. New Jersey’s local score is represented as a negative.

Sources: Sales Tax Clearinghouse; Tax Foundation calculations; State Revenue Department websites.

Avoidance of sales tax is most likely to occur in areas where there is a significant difference between jurisdictions’ rates. Research indicates that consumers can and do leave high-tax areas to make major purchases in low-tax areas, such as from cities to suburbs.[8] For example, evidence suggests that Chicago-area consumers make major purchases in surrounding suburbs or online to avoid Chicago’s 10.25 percent sales tax rate.[9]

At the statewide level, businesses sometimes locate just outside the borders of high sales-tax areas to avoid being subjected to their rates. A stark example of this occurs in New England, where even though I-91 runs up the Vermont side of the Connecticut River, many more retail establishments choose to locate on the New Hampshire side to avoid sales taxes. One study shows that per capita sales in border counties in sales tax-free New Hampshire have tripled since the late 1950s, while per capita sales in border counties in Vermont have remained stagnant.[10] At one time, Delaware actually used its highway welcome sign to remind motorists that Delaware is the “Home of Tax-Free Shopping.”[11]

State and local governments should be cautious about raising rates too high relative to their neighbors because doing so will yield less revenue than expected or, in extreme cases, revenue losses despite the higher tax rate.

This report ranks states based on tax rates and does not account for differences in tax bases (e.g., the structure of sales taxes, defining what is taxable and nontaxable). States can vary greatly in this regard. For instance, most states exempt groceries from the sales tax, others tax groceries at a limited rate, and still others tax groceries at the same rate as all other products.[12] Some states exempt clothing or tax it at a reduced rate.[13]

Tax experts generally recommend that sales taxes apply to all final retail sales of goods and services but not intermediate business-to-business transactions in the production chain. These recommendations would result in a tax system that is not only broad-based but also “right-sized,” applying once and only once to each product the market produces.[14] Despite agreement in theory, the application of most state sales taxes is far from this ideal.[15]

Hawaii has the broadest sales tax in the United States, but it taxes many products multiple times and, by one estimate, ultimately taxes 119 percent of the state’s personal income.[16] This base is far wider than the national median, where the sales tax applies to 36 percent of personal income.[17]

Sales Tax Clearinghouse publishes quarterly sales tax data at the state, county, and city levels by ZIP code. We weight these numbers according to Census 2010 population figures to give a sense of the prevalence of sales tax rates in a particular state.

It is worth noting that population numbers are only published at the ZIP code level every 10 years by the U.S. Census Bureau, and that editions of this calculation published before July 1, 2011, do not utilize ZIP code data and are thus not strictly comparable. ZIP code level data for the 2020 Census is not yet available, so the current edition continues to use 2010 Census numbers.

It should also be noted that while the Census Bureau reports population data using a five-digit identifier that looks much like a ZIP code, this is actually what is called a ZIP Code Tabulation Area (ZCTA), which attempts to create a geographical area associated with a given ZIP code. This is done because a surprisingly large number of ZIP codes do not actually have any residents. For example, the National Press Building in Washington, D.C., has its own ZIP code solely for postal reasons.

For our purposes, ZIP codes that do not have a corresponding ZCTA population figure are omitted from calculations. These omissions result in some amount of inexactitude but overall do not have a palpable effect on resultant averages because proximate ZIP code areas which do have ZCTA population numbers capture the tax rate of those jurisdictions.

Sales taxes are just one part of an overall tax structure and should be considered in context. For example, Tennessee has high sales taxes but no income tax, whereas Oregon has no sales tax but high income taxes. While many factors influence business location and investment decisions, sales taxes are something within policymakers’ control that can have immediate impacts.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

[1] Special taxes in Montana’s resort areas are not included in our analysis.

[2] This number includes mandatory add-on taxes which are collected by the state but distributed to local governments. Because of this, some sources will describe California’s sales tax as 6.0 percent. A similar situation exists in Utah and Virginia.

[3] The sales taxes in Hawaii and South Dakota have bases that include many services and so are not strictly comparable to other sales taxes.

[4] This rate includes two levies, summing 1.25 percentage points, which are imposed statewide but distributed to localities. See “Second Quarter 2019 Changes,” Utah State Tax Commission, Apr. 1, 2019, https://tax.utah.gov/sales/ratechanges.

[5] Illinois ranks 8th highest, a slight improvement from 7th highest in the July 2021 rankings, but this is due to an error in the source data on which we relied for the July effective rate calculations which has since been corrected, and not to any change in sales tax rates.

[7] Kacen Bayless, “Beaufort Co. voters say no to sales tax, government change in lopsided election,” The Island Packet (Bluffton, S.C.), Nov. 3, 2021, https://www.islandpacket.com/news/politics-government/election/article255479436.html.

[8] Scott R. Baker, Stephanie Johnson, and Lorenz Kueng, “Shopping for Lower Sales Tax Rates,” National Bureau of Economic Research Working Paper 23665, May 2018, https://www.nber.org/papers/w23665. See also Mehmet Serkan Tosun and Mark Skidmore, “Cross-Border Shopping and the Sales Tax: A Reexamination of Food Purchases in West Virginia,” Research Paper 2005-7, Regional Research Institute, West Virginia University, September 2005, https://researchrepository.wvu.edu/rri_pubs/109/, and T. Randolph Beard, Paula A. Gant, and Richard P. Saba, “Border-Crossing Sales, Tax Avoidance, and State Tax Policies: An Application to Alcohol,” Southern Economic Journal 64:1 (July 1997), 293-306.

[10] Arthur Woolf, “The Unintended Consequences of Public Policy Choices: The Connecticut River Valley Economy as a Case Study,” Northern Economic Consulting, Inc., November 2010, http://www.documentcloud.org/documents/603373-the-unintended-consequences-of-public-policy.html.

[12] For a list, see Janelle Cammenga and Jared Walczak, 2022 State Business Tax Climate Index, Tax Foundation, Dec. 16, 2021, https://taxfoundation.org/2021-state-business-tax-climate-index/.

[13] Liz Malm and Richard Borean, “How Does Your State Sales Tax See That Blue and Black (or White and Gold) Dress?” Tax Foundation, Feb. 27, 2015, http://taxfoundation.org/blog/how-does-your-state-sales-tax-see-blue-and-black-or-white-and-gold-dress.

[14] Justin M. Ross, “A Primer on State and Local Tax Policy: Trade-Offs among Tax Instruments,” Mercatus Center at George Mason University, Feb. 25, 2014, http://mercatus.org/publication/primer-state-and-local-tax-policy-trade-offs-among-tax-instruments.

[15] For a representative list, see Jared Walczak and Janelle Cammenga, 2021 State Business Tax Climate Index.